Featured Vendor

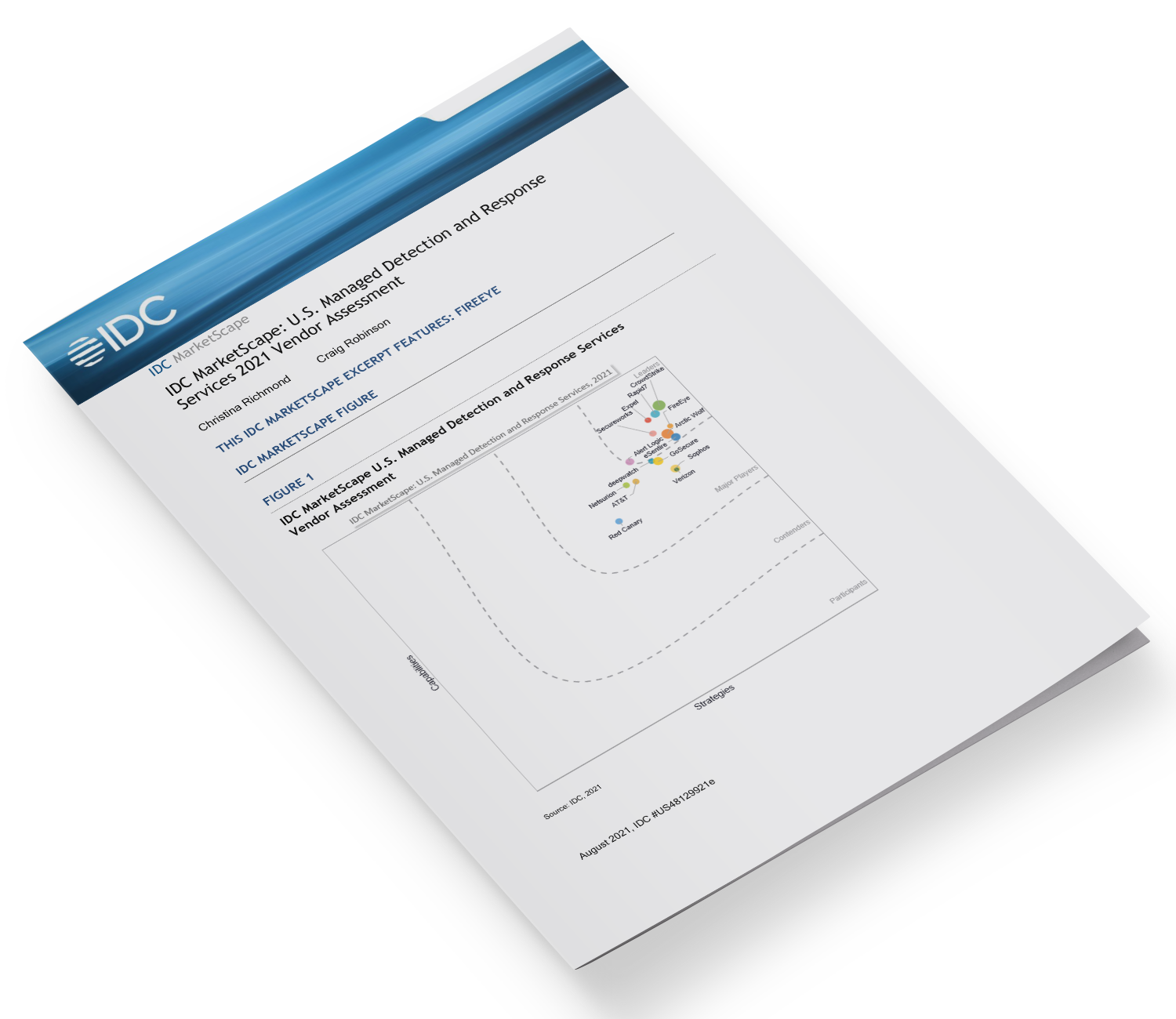

FireEye is positioned in the Leaders category in the 2021 IDC MarketScape for U.S. managed detection and response services. The evaluation of FireEye (Mandiant) was done prior to the June 3, 2021, announcement of the separation of the Mandiant offerings from FireEye. Henceforth, this vendor profile refers to the combined company as FireEye/Mandiant and the service offering by the Mandiant name.

FireEye was founded in 2004 and maintains headquarters in Milpitas, California. The company maintains SOCs in Reston, Virginia (global 24 x 7 x 365) and Dublin, Ireland; Singapore; and Sydney, Australia (all operate in the follow-the-sun model).

Mandiant Managed Defense is a managed detection and response service that includes four offerings: Managed Defense Nights and Weekends, Managed Defense for Endpoint Security, Managed Defense for Microsoft Defender for Endpoint, and Managed Defense for Operational Technology. All offerings include some combination of endpoint, network, email, and SIEM technology. The service provides 24 x 7 monitoring, alert disposition, containment, remediation recommendations, threat hunting (customizable by industry), rapid response, and guidance and insights.

Investigation and threat hunting are linked to Mandiant Threat Intelligence through the Mandiant Advantage Platform for added context and transparency. Active attacker–focused investigations can be conducted with or for customers on their behalf. Investigation reports and response activities are viewable in the portal.

MDR can be augmented with Mandiant Services, the Mandiant Advantage Platform offering, and Expertise On Demand, which provides access to Mandiant resources, supplemental intelligence, consulting, and training options. The Mandiant Advantage Platform enables customers to integrate their chosen offerings, such as additional threat intelligence, security validation, and automated defense.